Startup Valuation for Fundraising in India: A Comprehensive Guide for Founders in 2026

Startup valuation is one of the most consequential yet least understood elements of the fundraising process in India. Many first-time founders treat it as a mathematical exercise, leaning on peer benchmarks or simple formulas to arrive at a number. In practice, valuation is a carefully negotiated outcome shaped by business fundamentals, prevailing market conditions, investor conviction, and your ability to present a compelling, evidence-backed vision.

Whether you are preparing for a seed round, Series A, or Series B, getting your valuation right is far more strategic than simply pushing for the highest possible figure. It demands a careful balance between immediate capital needs, long-term founder equity, realistic growth expectations, and the ability to sustain momentum through future rounds.

An inflated valuation can deliver short-term validation, but it creates benchmarks that are difficult to meet, often resulting in down rounds, strained investor relationships, or unnecessary operational pressure. Conversely, an undervalued deal leads to excessive dilution, reduced control, and diminished founder motivation over time.

This guide walks through how startup valuation works within India's fundraising landscape, what experienced investors actually evaluate, how different methodologies apply, and what founders should do to position themselves effectively in 2026.

What Is Startup Valuation and Why Does It Matter in the Indian Context?

Startup valuation is the process of estimating the economic worth of a privately held company that does not have a liquid public market for its shares. Unlike listed companies, where daily trading determines share prices, startup valuations are inherently forward-looking and subjective. They depend on projected growth, risk assessment, and investor conviction rather than historical performance alone.

In India, valuation typically serves three distinct purposes:

- Fundraising valuation: The negotiated pre-money or post-money value agreed upon during investment rounds.

- Compliance valuation: Mandated under various regulatory frameworks for share issuances and foreign investments.

- ESOP valuation: Determines the fair market price for granting employee stock options, with direct implications for taxation and accounting.

Analytical frameworks such as Discounted Cash Flow (DCF), comparable company analysis, or the Venture Capital Method provide structure to this process. However, the final number almost always emerges from negotiation and the investor's assessment of the opportunity's risk-reward profile.

All valuation reports prepared for regulatory, or compliance purposes must be certified by IBBI-registered Registered Valuers and/or SEBI-registered Category I Merchant Bankers. These reports are customized to the client's specific objective, whether for equity fundraising, FEMA compliance, ESOP issuance, or regulatory filings.

Funding data from 2025 through early 2026 indicates that India's startup funding environment has matured significantly. While overall venture capital deployment showed resilience, investors have grown markedly more disciplined. Seed funding saw compression in volume. Series A and B round now resemble what was previously expected at later stages, with greater emphasis on proven traction and sustainable metrics. Median valuations have stabilized, but a clear divide has emerged between top-quartile companies that command premiums and others facing flat or down rounds.

The Strategic Importance of Getting Valuation Right

Valuation decisions made today carry compounding effects throughout your startup journey. Here are why founders must approach this with deliberate intent:

1. Dilution Compounds Across Funding Rounds

Every new investment dilutes existing shareholders, particularly founders. A seemingly small difference, such as giving up 22% equity instead of 18% at the seed stage, can translate into millions of rupees in lost value at exit. Across multiple rounds, these gaps widen substantially, directly affecting both founder control and financial upside.

2. It Sets the Benchmark for Subsequent Raises

Your current valuation becomes the reference point for future negotiations. If the business fails to demonstrate sufficient progress, founders' risk flat rounds (no valuation increase), down rounds (lower valuation triggering anti-dilution clauses), or damaged credibility with existing and prospective investors.

3. Investor Expectations Scale with Valuation

A higher entry valuation signals strong conviction but also imposes elevated performance expectations. Investors will anticipate accelerated revenue growth, improving unit economics, better capital efficiency, and a clearer trajectory toward profitability or significant scale. Falling short can erode trust and complicate follow-on funding considerably.

In the current 2026 environment, where capital allocation is selective and investors prioritize quality over quantity, these considerations have become even more critical. Many founders are raising larger early-stage checks to secure longer runways, sometimes accepting higher dilution earlier to avoid funding gaps.

What Indian Investors Actually Prioritize in 2026

While founders tend to fixate the headline valuation number, seasoned investors focus on the underlying drivers of sustainable value creation. In today's market, conviction stems less from hype and more from verifiable fundamentals.

1. Revenue Quality and Predictability

Investors look beyond headline revenue figures to analyze composition. Recurring revenue streams, strong customer retention (with net revenue retention ideally exceeding 110% in SaaS models), consistent month-on-month growth, and stable long-term B2B contracts command premium attention. Predictable, high-quality revenue reduces risk and improves forecasting accuracy, which directly supports higher valuation of multiples.

2. Addressable Market Opportunity

A sizable Total Addressable Market (TAM) remains essential, but sophisticated investors demand granular breakdowns: Serviceable Available Market (SAM) and Serviceable Obtainable Market (SOM). They expect realistic, bottom-up projections of market capture over three to five years, supported by credible data rather than generic industry reports.

3. Founder and Leadership Team Strength

Particularly at seed and early Series A stages, investors continue to bet heavily on people. Domain expertise, prior execution experience, the ability to attract top talent, and a complementary leadership team can justify higher valuations even when financial traction is still building.

4. Capital Efficiency and Burn Discipline

Post the funding corrections of recent years, capital efficiency has become a non-negotiable criterion. Investors closely examine burn rate relative to growth, customer acquisition costs (CAC), payback periods, and revenue generated per unit of capital invested. A startup achieving Rs. 2 to 3 crore ARR with controlled burn is viewed far more favorably than one generating similar revenue through heavy spending.

5. Unit Economics

Sustainable unit economics form the foundation for long-term scalability. Key metrics include gross margins, contribution margins, customer lifetime value (LTV), and the LTV-to-CAC ratio, ideally at 3:1 or higher. In 2026, many investors expect clear evidence of improving economics or a well-defined path to breakeven within 18 to 24 months.

6. Competitive Moat and Defensibility

Investors want assurance that the business can protect its margins and market position. Potential moats include proprietary technology, network effects, brand strength, high switching costs, or unique distribution advantages. Without a discernible moat, startups face constant pricing pressure that compresses valuations.

7. Growth Trajectory and Sustainability

High growth rates remain attractive, but only when underpinned by quality metrics. Month-on-month momentum combined with improving retention and economics carries significant weight.

8. Realistic Path to Exit

Ultimately, investors evaluate potential returns. They assess acquisition opportunities, IPO feasibility, sector consolidation trends, and the likelihood of achieving their target multiples, often 10x or more over five to seven years. A credible exit narrative meaningfully strengthens the valuation of discussions.

In SaaS and fintech, revenue multiples in private deals have stabilized in the 8x to 15x ARR range depending on growth and margins. Edtech and consumer models often trade at lower multiples unless they demonstrate exceptional defensibility.

Valuation Methods Commonly Applied in Indian Fundraising

Several established approach's structure valuation discussions, though the final figure remains negotiation-driven:

- Comparable Company Analysis This method benchmarks the startup against recent deals or public peers using revenue multiples, ARR multiples, or EBITDA where applicable. Adjustments account for differences in growth rate, geography, business model, and stage.

- Discounted Cash Flow (DCF) DCF projects future cash flows and discounts them to present value. This approach is more relevant for later-stage companies with greater cash flow visibility. It is less reliable for early-stage ventures due to high uncertainty in projections.

- Venture Capital Method This approach works backward from an estimated terminal value at exit, applying the investor's required return multiple and desired ownership percentage. It closely mirrors how many venture capitalists internally evaluate opportunities.

- Qualitative Early-Stage Methods For pre-revenue or very early startups, frameworks like the Berkus Method, Scorecard Method, or Risk Factor Summation assign value based on qualitative factors such as team strength, prototype development, and market risk.Professional valuation exercises typically blend multiple methods for robustness. All such reports must be certified by Registered Valuers or Merchant Bankers to ensure regulatory acceptance in India.

Stage-by-Stage Valuation Benchmarks: Seed, Series A, and Series B in India

One dimension that founders frequently overlook is how valuation expectations and methods shift dramatically across funding stages. Understanding these stage-specific norms helps you calibrate your request and structure your data room more effectively.

Seed Stage (Rs. 50 lakhs to Rs. 5 crores raised)

At this stage, financial history is often minimal. Valuation is heavily influenced by the founding team's credibility, the clarity of the problem being solved, early product validation, and the perceived size of the addressable opportunity. Qualitative methods like the Scorecard Method and Berkus Method are common. Pre-money valuations in India at seed stage typically range from Rs. 5 crores to Rs. 25 crores depending on sector, team pedigree, and early traction.

Investors at this stage also evaluate the founder's understanding of unit economics, even if formal data is limited. Showing awareness of how the business will eventually generate sustainable margins signals maturity.

Series A (Rs. 5 crores to Rs. 50 crores raised)

By Series A, investors expect meaningful proof points. These include a product that has found initial market fit, a repeatable customer acquisition process, and early signals of positive unit economics. Revenue multiples become central to the negotiation, with ARR multiples ranging from 8x to 20x depending on growth rate and category.

In 2026, Series A investors in India expect what was previously associated with Series B, including meaningful monthly recurring revenue, low churn, and a clear path to operational leverage. Valuations at this stage typically range from Rs. 40 crores to Rs. 200 crore pre-money for high-quality businesses.

Series B (Rs. 50 crores to Rs. 250 crores raised)

At Series B, the DCF methodology becomes increasingly relevant because the business has sufficient operating history to model future cash flows with some defensibility. Comparable transaction analysis also plays a larger role. Investors scrutinize gross margin trends, sales cycle efficiency, and net revenue retention closely.

Pre-money valuations vary widely, but Series B rounds in India in 2025 to 2026 have typically ranged from Rs. 200 crores to Rs. 1,000 crores for companies with strong fundamentals and category leadership.

Understanding where your business sits on this spectrum helps you avoid the common mistake of applying seed-stage logic to a Series A negotiation or vice versa.

Pre-Money vs Post-Money Valuation and the Impact of ESOP Pools

Founders must clearly understand the distinction between these two concepts and their practical implications:

- Pre-money valuation: The company's estimated worth immediately before the new investment is received.

- Post-money valuation: Pre-money valuation plus the amount of fresh capital injected.

Investor ownership percentage is calculated as: Investment Amount divided by Post-Money Valuation.

Employee Stock Option Plans (ESOPs) introduce an additional layer of complexity. Option pools are frequently established or expanded before a funding round is closed. Because this dilution typically comes from existing shareholders, often founders, it allows investors to receive their full negotiated stake on a post-pool, post-money basis.

Founders should negotiate pool size thoughtfully, aligning it with realistic hiring roadmaps while modeling cumulative dilution across multiple future rounds. Poor planning at this stage can lead to unexpected and significant erosion of founder equity, particularly when combined with the dilution from the funding round itself.

A clean, transparent capitalization table that accurately reflects current ownership, option pools, and any outstanding convertible instruments is essential before entering any valuation of discussion.

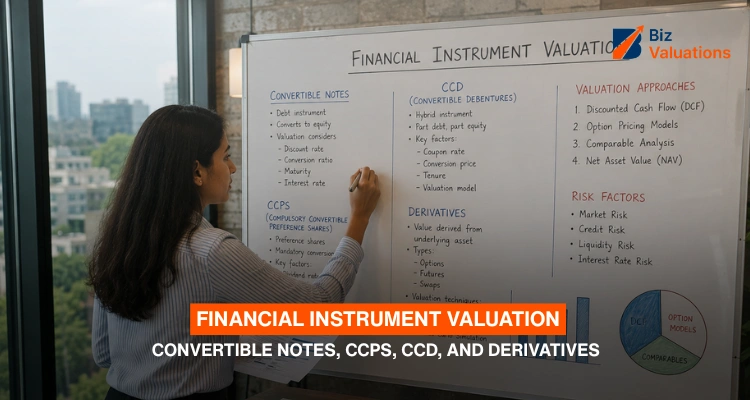

How Convertible Instruments Affect Your Startup Valuation

This is a section many startup guides in India overlook, yet it has a direct bearing on your effective valuation and cap table at the time of a priced round.

Convertible instruments, including SAFE (Simple Agreement for Future Equity) notes, Compulsorily Convertible Debentures (CCDs), and Compulsorily Convertible Preference Shares (CCPS), are widely used in Indian startup financing, particularly at the pre-seed and seed stages.

How Convertibles Impact Valuation

When a SAFE or CCD converts at the time of a priced round, it converts a discount to the round valuation (typically 15% to 25%) or at a valuation cap, whichever is more favorable to the investor. This conversion happens before the new round is priced, meaning founders experience additional dilution that is not always immediately visible in early negotiations.

For example, if you raised Rs. 2 crores via a SAFE with Rs. 20 crore cap and then raise a Series A at Rs. 50 crore pre-money; the SAFE converts at Rs. 20 crores (the cap), giving that investor a larger ownership stake than a Series A investor putting in the same amount. This dilution directly reduces what the Series A price implies for founder equity.

Regulatory Considerations

Under Indian regulations, convertible instruments issued to foreign investors must comply with FEMA guidelines and the RBI's pricing norms. The valuation at issuance and conversion must be certified by an IBBI Registered Valuer or a SEBI Category I Merchant Banker. CCDs and CCPS issued to foreign investors also require FC-GPR filings, making proper valuation documentation non-negotiable.

Biz Valuations provides valuations for convertible instruments structured for both domestic compliance under the Companies Act and cross-border compliance under FEMA and SEBI regulations.

Practical Advice for Founders

Before your next priced round, run a full cap table simulation that accounts for all outstanding convertible instruments and their conversion terms. This exercise often reveals that the effective dilution from a new round is meaningfully higher than the headline percentage suggests.

Regulatory Framework Governing Valuation in India

India's regulatory environment adds important compliance dimensions to every valuation exercise:

Companies Act, 2013

Section 247 of the Companies Act requires valuation by a Registered Valuer for a range of share-related transactions, including preferential allotments and ESOP grants. Non-compliance can render transactions invalid or attract regulatory scrutiny.

FEMA Regulations

Foreign direct investment must generally occur at or above fair market value as certified by an eligible valuer. Proper valuation reports are mandatory for FC-GPR filings and related RBI compliances. For FDI transactions exceeding USD 5 million, only a SEBI Category I Merchant Banker is authorized to certify the Fair Market Value.

Income Tax Act

Rules around fair market value under Rule 11UA affect the taxation of ESOPs and share issuances, with specific implications for Section 56(2) and angel tax provisions. While DPIIT-recognized startups have received relief from certain provisions, the Rule 11UA framework continues to apply to a large universe of companies.

Ensuring full compliance is non-negotiable. All valuation reports delivered by Biz Valuations are certified by IBBI-registered Registered Valuers and/or SEBI-registered Merchant Bankers, tailored precisely to the client's needs and the intended purpose, whether for domestic fundraising, inbound foreign investment, ESOP structuring, or regulatory filings. This approach minimizes regulatory risk and accelerates deal closure.

Common Pitfalls Founders Encounter During Valuation Discussions

Even promising startups stumble due to avoidable errors. Here are the most frequent ones:

1. Setting Unrealistically High Valuations

Over-optimism deters serious investors or creates unsustainable benchmarks that lead to down-rounds. A valuation you cannot grow is more damaging than one that appears conservative today.

2. Over-Reliance on Vanity Metrics

Focusing on downloads, app installs, or social media followers rather than revenue quality, retention, and unit economics rarely impresses experienced investors in 2026.

3. Inadequate Modeling of Dilution

Failing project ownership across multiple rounds, including the impact of ESOP pools and outstanding convertible instruments, results in unpleasant surprises at later stages.

4. Weak Financial Preparation

Incomplete models, unrealistic assumptions, or the absence of audited statements undermine credibility at a critical moment in investor discussions.

5. Accepting the First Term Sheet Without Alternatives

Without competitive tension from multiple term sheets, founders lose negotiating leverage on valuation and other key terms.

6. Ignoring Sector-Specific Benchmarks

Not understanding current valuation of multiples or investor expectations for your specific industry can lead to misaligned asks that immediately signal a lack of market awareness.

In 2026, additional risks include raising overly large early checks that inflate future dilution expectations or failing to demonstrate improving unit economics amid increasingly selective capital allocation.

Best Practices for Preparing Strong Valuation Discussions

Founders who approach valuation strategically consistently achieve better outcomes. Here are the essential steps:

- Build a Robust, Assumption-Driven Financial Model Develop detailed projections with clear, defensible assumptions around revenue drivers, cost structures, and key milestones. Include base, upside, and conservative scenarios to demonstrate analytical rigor.

- Maintain a Clean and Transparent Capitalization Table Your cap table should accurately reflect current ownership, option pools, and all outstanding convertible instruments. Transparency builds trust and speeds up due diligence.

- Assemble a Comprehensive Data Room Organize legal documents, financial statements, customer contracts, IP details, operational metrics, and compliance records in an accessible and well-structured format before initiating investor conversations.

- Craft a Credible Growth Narrative Clearly explain the problem you solve, your unique approach, your path to scale, and how you will create substantial value. Support every claim with data rather than aspiration alone.

- Benchmark Realistically Research recent comparable deals in your sector and stage. Align your valuation with achievable milestones and demonstrated traction, not peer rumors or headline funding stories.

- Engage Professional Support Early Work with experienced advisors and certified valuers to strengthen your position and ensure regulatory readiness well before investor conversations begin. Three questions every founder should be able to answer clearly: What valuation can you realistically defend with current data and near-term milestones? What level of dilution are you prepared to accept? Can the business demonstrably grow into this valuation before the next round becomes necessary?

Sector Trends and Valuation Realities in 2026

The Indian startup market continues to demonstrate resilience, with funding concentrated in companies that exhibit strong fundamentals. Fintech and SaaS have remained relatively active, while AI-integrated solutions across verticals attract growing attention when paired with clear distribution advantages and improving economics.

Early-stage valuations have been stabilized. Seed rounds often range between Rs. 15 crore and Rs. 30 crore pre-money depending on traction, and Series A medians reflect more disciplined multiples than the peak years of 2021 to 2022.

Investors now expect Series A companies to show what was previously required at Series B levels: meaningful revenue, repeatable sales processes, and healthy unit economics. This shift rewards disciplined execution and punishes over-hyped but under-proven models.

For sectors such as climate tech, deep tech, and AI applications, valuations are increasingly tied to the clarity of the problem being solved and the defensibility of the technology, rather than speculative projections. Investors in these categories apply greater scrutiny to IP ownership, technical differentiation, and go-to-market strategy.

Conclusion: Building Value Beyond the Number

In India's maturing startup ecosystem, valuation is never determined by formulas in isolation. It emerges at the intersection of robust business fundamentals, including revenue quality, capital efficiency, unit economics, team capability, market opportunity, and competitive defensibility, combined with investor perception and broader market dynamics.

Rather than treating valuation as the ultimate goal of a fundraising process, successful founders view it as one important milestone on the path to building a sustainable, scalable enterprise. Those who prioritize genuine value creation, maintain disciplined operations, and communicate transparently consistently secure more favorable terms and form stronger long-term investor partnerships.

Whether you are approaching your first institutional round or preparing for a later-stage raise, ensuring your valuation is well-supported, compliance-ready, and backed by a certified report from an IBBI Registered Valuer strengthens your position considerably.

Biz Valuations offers startup valuation services certified by IBBI Registered Valuers and SEBI Category I Merchant Bankers, covering everything from seed-stage ESOP valuation to Series B fundraising reports and FEMA compliance for FDI transactions. With 3,500+ certified valuations, 15+ years of expertise, and a 7 to 10 working day turnaround, we are the independent valuation partner that founders, investors, and regulators trust.

Frequently Asked Questions (FAQs)

Mr. Saurobh Barick

Registered Valuer (IBBI) & Valuation Expert

DCF & Fair Market Value Valuations | FEMA, Income Tax & Companies Act | 409A Valuation | M&A, Fundraising valuation | Cross-Border & Startup/Business Valuation | SME IPO AdvisorySaurobh Barick is a Registered Valuer with the Insolvency and Bankruptcy Board of India (IBBI) and a finance professional with over 15 years of experience in valuation and financial advisory services.