Merger Valuation Explained: Methods, Models, and Real-World Applications in M&A

In the world of corporate transactions, merger valuation is the single most important analytical exercise a deal team will undertake. Get it right, and the merger creates genuine shareholder value. Get it wrong, and the acquiring company spends years writing down goodwill and explaining to investors why the deal made sense on paper but not in practice.

Merger valuation is not a simple formula or a spreadsheet exercise. It combines rigorous financial modelling with strategic thinking, regulatory awareness, and a clear-eyed view of what two businesses can genuinely achieve together versus what they each achieve alone.

This guide breaks down every essential element of merger valuation: the core concepts, the established methods, the advanced models, the regulatory landscape in India, and the lessons drawn from landmark transactions. Whether you are a CFO preparing an acquisition, an investment banker structuring a deal, or a business owner evaluating strategic options, you will find practical frameworks here to navigate the complexity of M&A pricing.

What Is Merger Valuation and Why Does It Matter?

Merger valuation is the systematic process of determining the economic worth of the entities involved in a proposed business combination. It moves beyond a simple standalone appraisal by factoring in the strategic rationale of the deal, the integration benefits expected from combining operations, and the unique risks that arise when two organizations merge into one.

At its core, merger valuation serves three practical purposes. First, it establishes a defensible purchase price that both parties and their advisors can justify. Second, it informs the exchange ratio in all-stock or mixed consideration deals, determining how many shares of the acquiring company a target shareholder receives per share they hold. Third, it provides a forward-looking framework to evaluate whether the transaction will be earnings-accretive and deliver adequate returns on the capital deployed.

In an era of heightened regulatory scrutiny, volatile capital markets, and rapid technological change, accurate valuation has never been more critical. Unlike a standard equity appraisal, merger analysis adopts a dual perspective: the intrinsic standalone value of each entity and the incremental value created by bringing them together.

Fundamental Concepts Every Deal Professional Must Understand

Enterprise Value vs. Equity Value

Deal professionals work primarily with Enterprise Value (EV), which represents the total economic value of a business's operating assets. It is calculated as market capitalization plus net debt (total debt minus cash and equivalents). EV allows for a like-for-like comparison across companies with different capital structures, which is essential in M&A analysis.

Equity value, by contrast, reflects only the residual claim belonging to shareholders after all creditor obligations are settled. In most acquisitions, the buyer assumes the target debt, making EV the relevant headline metric. Further adjustments for non-operating assets, contingent liabilities, and working capital normalize the picture before negotiations begin.

The Power and Peril of Synergies

Synergies represent the additional value unlocked by combining two businesses, and they are typically the primary justification for paying a premium over standalone value. They fall into three broad categories:

- Cost synergies arise from procurement savings, headcount rationalization, facility consolidation, and integration of technology platforms.

- Revenue synergies are driven by cross-selling opportunities, expanded geographic reach, stronger product portfolios, or improved pricing power.

- Financial synergies include optimized capital structures, lower borrowing costs from improved credit profiles, and tax efficiencies such as utilization of carried-forward losses.

The discipline lies in quantifying synergies honestly. Historical M&A data consistently shows that many deals fail to deliver their projected benefits, typically because synergy estimates were overly optimistic, or execution was underestimated. Cost synergies achieve realization rates of 70 to 80%, while revenue synergies often fall below 50%.

Control Premium and What It Reflects

Acquirers almost always pay a control premium over the target's pre-announcement market price, commonly ranging from 20% to 40%. This premium reflects the value of gaining decision-making authority: the ability to direct strategy, restructure operations, replace management, and capture synergies unavailable to minority shareholders. In competitive auction processes, premiums can climb significantly higher, which is exactly where valuation discipline becomes most important.

Accretion and Dilution Analysis

Every public company acquisition is evaluated for its impact on the acquirer's earnings per share (EPS). An accretive deal increases EPS; a dilutive one reduces it, at least in the near term. Sophisticated models project pro forma financials over multiple years, incorporating financing costs, phased synergy realization, and integration expenses to assess long-term value creation rather than just the first-year headline.

Core Merger Valuation Methods: The Building Blocks of M&A Analysis

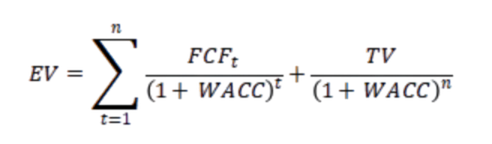

Discounted Cash Flow (DCF) Analysis

DCF is widely regarded as the most rigorous intrinsic valuation technique in M&A. It estimates the present value of a business based on its projected future free cash flows, discounted at the Weighted Average Cost of Capital (WACC).

The basic structure is:

Where FCFt is the free cash flow in each forecast period and Terminal Value captures the ongoing value of the business beyond the explicit forecast window, typically five to ten years.

DCF's strength lies in its forward-looking orientation and its ability to incorporate company-specific risks through beta, cost of equity, and explicit growth assumptions. Its limitation is sensitivity: small changes in terminal growth rate or WACC can shift the concluded value substantially, which is why thorough sensitivity analysis and scenario testing are non-negotiable components of any credible DCF.

Comparable Company Analysis (Trading Multiples)

This relative valuation approach benchmarks the target against publicly listed peers using valuation multiples such as EV/EBITDA, Price/Earnings (P/E), EV/Revenue, or Price/Book.

For example, if comparable firms in the pharmaceutical sector trade at an average EV/EBITDA of 15x and the target generates Rs. 200 crores in EBITDA, a preliminary enterprise value of Rs. 3,000 crore emerges. Adjustments follow for differences in growth prospects, margins, risk profiles, and market positioning.

This method benefits from market efficiency and real-time pricing signals. Its limitation is the difficulty of finding genuinely comparable companies, particularly in niche or rapidly evolving industries. Market sentiment can also distort multiples during boom or bust cycles, making contextual judgement essential.

Precedent Transaction Analysis

Precedent transaction analysis examines prior M&A deals in the same or adjacent sectors to identify the prices actually paid in negotiated transactions, including control premiums and synergy expectations embedded in those prices. Data sources include deal databases, regulatory filings, and press releases disclosing transaction multiples.

Because past deals reflect real negotiated outcomes rather than theoretical trading levels, precedent analysis often provides a realistic ceiling or floor for current negotiations. The key challenge is adjusting for unique circumstances in historical transactions, changes in market conditions, and deal-specific factors that may not apply to the current situation.

Asset-Based and Replacement Cost Approaches

These approaches are particularly relevant for asset-intensive industries such as manufacturing, real estate, and natural resources. They value the underlying assets and liabilities individually, using adjusted book value, liquidation value, or reproduction cost less depreciation.

In most going-concern mergers, asset-based approaches serve as a supplementary floor rather than the primary method, because they tend to undervalue intangible assets and future earnings potential. In distressed situations or asset-heavy deals, however, they carry significant weight.

How Exchange Ratios Are Determined in Indian Mergers

In India, determining the share exchange ratio is one of the most scrutinized aspects of any merger. Under Sections 230 to 232 of the Companies Act 2013, companies undertaking a merger or demerger must obtain independent valuation reports from IBBI Registered Valuers, and these reports directly inform the exchange ratio presented to shareholders and submitted to the National Company Law Tribunal (NCLT) for approval.

The exchange ratio is calculated by dividing the per-share value of the target by the per-share value of the acquirer, adjusted for any cash components or additional premiums. For listed companies, SEBI additionally requires that the ratio be supported by a fairness opinion from a SEBI Category I Merchant Banker, adding a second layer of regulatory verification.

A well-constructed exchange ratio reflects not only current market prices and intrinsic values but also the relative contribution of each entity to the combined business, projected post-merger synergies, and the long-term earnings profile of the merged entity. Mispricing the ratio creates shareholder disputes and exposes boards to legal and regulatory challenges.

The HDFC Bank and HDFC Ltd merger in 2023, which used an exchange ratio of 42:25, is the most prominent recent example of how complex this exercise becomes when both entities are large, regulated, and heavily scrutinized.

The Regulatory Framework for M&A Valuations in India

India's M&A valuation landscape is shaped by a layered regulatory architecture that practitioners must navigate carefully. The key frameworks are:

- Companies Act 2013: Mergers, demergers, and amalgamations require independent valuation reports from IBBI Registered Valuers. Reports must be filed with the NCLT, ROC, and submitted to shareholders.

- SEBI Regulations: For transactions involving listed companies, including preferential allotments, open offers, buybacks, and related-party transactions, SEBI mandates valuation by a Category I Merchant Banker. This applies to fairness of opinions for schemes involving listed entities.

- Income Tax (Rule 11UA): Share issuances at a premium in unlisted companies require Fair Market Value certification to avoid Section 56(2) angel tax exposure. DPIIT-recognized startups received relief under 2023 amendments, but the requirement continues to apply broadly.

- FEMA / FDI Regulations: Cross-border share transfers require RBI-compliant FMV certification. For FDI transactions exceeding USD 5 million, only a SEBI Category I Merchant Banker can certify the Fair Market Value.

- Ind-AS / IFRS: Post-merger financial reporting requires Purchase Price Allocation (PPA) under Ind-AS 103, goodwill impairment testing under Ind-AS 36, and fair value measurements under Ind-AS 113.

Biz Valuations holds both IBBI Registered Valuer status and SEBI Category I Merchant Banker registration, making it one of the few firms in India equipped to handle all five regulatory valuation requirements under a single engagement. With 3,500+ certified valuations delivered across 35+ industries, Biz Valuations brings the regulatory depth and audit-ready documentation that NCLT submissions and SEBI filings demand.

Determining the Swap Ratio

Private equity sponsors rely on LBO models to determine the maximum purchase price that still delivers their target internal rate of return, typically between 20% and 30%. These models layer substantial debt onto the target balance sheet, project deleveraging through operational cash flows, and assume an exit multiple after a holding period of three to seven years. Key outputs include IRR, cash-on-cash returns, and debt coverage ratios for lenders.

Merger Consequences (Accretion/Dilution) Models

These integrated models combine the balance sheets and income statements of both entities on a pro-forma basis. They simulate various financing structures, whether cash, stock, or debt, and layer in phased synergy realization alongside one-time integration costs. The output guides decisions on the optimal consideration mix and helps communicate the value creation thesis to investors and analysts.

Sum-of-the-Parts (SOTP) Valuation

Conglomerates and diversified businesses benefit from valuing each operating segment independently, using multiples or DCF assumptions tailored to that specific unit, and then aggregating the results. Holding company discounts or premiums may apply to reflect the overall conglomerate structure. SOTP is also frequently used to assess what a combined entity should be worth post-merger if certain divisions are sold off as part of the integration.

Landmark Deals: Valuation Lessons from Real Transactions

HDFC Bank and HDFC Ltd Merger (2023)

India's most significant banking merger involved an exchange ratio of 42 HDFC Bank shares for every 25 HDFC Ltd shares held. The valuation reflected not only market prices but also substantial synergies in funding costs, cross-selling of banking and housing finance products, and capital optimization at the regulatory level. This transaction demonstrated how long-term franchise value and regulatory capital efficiency can justify premium pricing in a heavily supervised sector.

Vodafone-Idea Merger

This telecom consolidation highlighted the importance of valuing spectrum assets, subscriber bases, and network infrastructure beyond traditional earnings multiples. Post-merger deleveraging and cost rationalization played central roles in the valuation thesis. The deal also demonstrated how industry-specific intangibles, particularly spectrum and subscriber retention, must be modelled carefully to avoid overvaluation.

Microsoft's Acquisition of LinkedIn (2016)

Valued at approximately USD 26.2 billion, the deal was a clear example of premium pricing for network effects, data assets, and ecosystem integration. Despite LinkedIn's modest profitability at the time of acquisition, Microsoft's valuation incorporated substantial revenue and productivity synergies across its Office suite and cloud platforms, validating a growth-oriented rather than earnings-based valuation framework.

Disney's Purchase of Pixar (2006)

The USD 7.4 billion transaction assigned high value to Pixar's creative talent, intellectual property pipeline, and cultural fit. Traditional DCF analysis would have struggled with uncertain future film revenues. Instead, strategic and qualitative factors drove the premium, illustrating that in creative and IP-intensive industries, conventional financial models must be supplemented with strategic scenario analysis.

Facebook (Meta) Acquisition of Instagram (2012)

Purchased for USD 1 billion when Instagram had minimal revenue, the valuation was built almost entirely on explosive user growth, long-term advertising potential, and defensive positioning against emerging rivals. This case remains one of the clearest examples of how platform economics and network effects can dominate conventional financial metrics in early-stage digital acquisitions.

Quantifying and Realizing Synergies: The Real Work of Merger Valuation

Effective synergy valuation isolates the incremental cash flows attributable specifically to the merger and discounts them at a higher hurdle rate to reflect execution risk. This is not a top-down estimate. It requires detailed bottom-up operational due diligence: identifying specific headcount redundancies, overlapping supplier contracts, shared technology platforms, and cross-selling pipeline opportunities.

Historical M&A experience shows that cost synergies achieve realization rates of 70 to 80%, while revenue synergies frequently fall below 50%. The implication is straightforward: build your base case on cost synergies, treat revenue synergies as upside, and stress-test for the scenario where they do not materialize.

Integration planning must begin during the valuation phase, not after signing. The gap between modelled synergy benefits and actual delivery is almost always rooted in integration planning that started too late.

Due Diligence and Its Impact on Merger Valuation

Due diligence is not a separate exercise from valuation. It is the foundation on which reliable valuation rests. Financial due diligence surfaces quality-of-earnings issues, working capital irregularities, off-balance-sheet liabilities, and revenue recognition practices that can materially change what a buyer should pay.

Legal due diligence identifies pending litigation, regulatory orders, and contractual restrictions that create contingent liabilities. Operational due diligence tests whether the synergies being assumed in the valuation model are actually achievable given the target's people, processes, and technology.

In Indian M&A transactions, regulatory due diligence has become increasingly important. Competition Commission of India (CCI) clearance thresholds, SEBI compliance status, IBBI registration validity, and pending NCLT proceedings all affect deal certainty and therefore deal value. A valuation built without thorough due diligence is, at best, a starting point and, at worst, a costly mistake.

Biz Valuations' approach integrates regulatory, financial, and operational context directly into the valuation framework, producing reports that reflect the real picture rather than the projected one.

Post-Merger Integration and Its Effect on Value Realization

One of the most consistent findings in M&A research is that poor post-merger integration destroys value that valuation models assumed would be created. McKinsey data suggests that between 50% and 60% of mergers fail to deliver their projected returns, with the primary causes being integration difficulties, cultural friction, and talent attrition at the target company.

From a valuation standpoint, this reality has two implications. First, integration costs must be explicitly modelled and deducted from synergy benefits. One-time restructuring charges, redundancy costs, system migration expenses, and advisory fees frequently amount to 3 to 5% of deal value. Second, the synergy ramp-up schedule must be realistic. Models that assume 100% synergy delivery within 12 months of closing are almost always wrong.

Valuations that account for integration risk with conservative phasing, higher discount rates on synergy cash flows, and explicit downside scenarios produce far more defensible and ultimately accurate conclusions.

Persistent Challenges in Merger Valuation

- Overoptimism bias: Management teams and advisors sometimes inflate growth projections or synergy estimates to make deals appear viable that would otherwise fail the financial test.

- Integration and cultural risks: Financial models rarely capture the human and organizational friction that erodes value during the months following a merger closing.

- Macroeconomic volatility: Interest rate shifts, currency fluctuations, and geopolitical events can render careful valuations obsolete within a matter of weeks.

- Information asymmetry: Private targets or complex conglomerates create data gaps that make assumptions less reliable and due diligence more demanding.

- Regulatory and antitrust considerations: CCI filings in India, NCLT approval timelines, and SEBI scrutiny all affect deal certainty and should be factored into probability-adjusted valuations.

Best Practices for Robust Merger Valuation

1. Triangulate using multiple methods to establish a valuation range rather than a single point estimate.

2. Apply conservative base-case assumptions with comprehensive sensitivity tables showing how value changes under different growth, margin, and discount rate scenarios.

3. Commission on independent fairness opinions wherever board conflicts of interest exist. In listed company transactions in India, SEBI makes this mandatory.

4. Align the valuation with a clearly articulated strategic thesis and a detailed integration roadmap that has been reviewed operationally, not just financially.

5. Stress-test for downside scenarios: synergy shortfalls, prolonged integration periods, and revenue attrition at the target.

6. Maintain transparent documentation to support board decisions, shareholder approvals, NCLT filings, and regulatory submissions.

Engaging experienced merchant bankers, IBBI Registered Valuers, and sector specialists early in the process enhances credibility and reduces the blind spots that often lead to overpayment.

Emerging Trends Shaping the Future of Merger Valuation

Artificial intelligence and machine learning are beginning to transform how deal teams approach comparable selection, financial anomaly detection, and preliminary synergy modelling. While these tools accelerate analysis, the judgment applied to their outputs remains a human responsibility.

Environmental, Social, and Governance (ESG) factors are increasingly influencing discount rates and long-term growth projections, particularly in industries where regulatory transition risks are high. Valuing digital assets, subscription businesses, and data platforms requires frameworks that go beyond traditional industrial models.

In India specifically, evolving IBBI regulations, SEBI guidelines for listed entity transactions, and competition law are continuously reshaping valuation standards. The rise of pre-IPO valuations driven by India's active IPO pipeline, and the growing use of complex convertible instruments in startup funding, are creating demand for increasingly sophisticated methodologies.

Conclusion: The Discipline That Separates Successful Deals from Cautionary Tales

Merger valuation is an equal part of analytical discipline and strategic judgment. DCF models, trading multiples, and precedent transaction analysis provide a rigorous framework. But experience, sector knowledge, regulatory awareness, and honest assumption-setting ultimately determine whether a concluded value will hold up in practice.

Deals anchored in realistic assumptions, disciplined synergy estimation, conservative integration modelling, and thorough regulatory due diligence consistently deliver better outcomes than those driven by deal momentum and inflated projections. The difference between a landmark success and a regretted transaction often lies in the honesty and depth applied during the valuation process itself.

Biz Valuations brings together IBBI Registered Valuer authority, SEBI Category I Merchant Banker credentials, and 3,500+ certified valuations across 35+ industries to deliver merger valuations that stand up to auditor, regulator, investor, and NCLT scrutiny. With a turnaround time of 7 to 10 working days and deep cross-regulatory expertise, Biz Valuations is the independent valuation partner that Indian deal teams trust.

Frequently Asked Questions (FAQs)

Mr. Saurobh Barick

Registered Valuer (IBBI) & Valuation Expert

DCF & Fair Market Value Valuations | FEMA, Income Tax & Companies Act | 409A Valuation | M&A, Fundraising valuation | Cross-Border & Startup/Business Valuation | SME IPO AdvisorySaurobh Barick is a Registered Valuer with the Insolvency and Bankruptcy Board of India (IBBI) and a finance professional with over 15 years of experience in valuation and financial advisory services.