Preferential Allotment Valuation Under Section 62 of Companies Act 2013: Complete Compliance Guide for Unlisted Companies

Raising capital through a targeted investor without going public is one of the most practical options available to Indian companies today. Preferential allotment under Section 62(1)(c) of the Companies Act, 2013 makes this possible. It allows private and unlisted companies to issue equity shares, convertible securities, or other instruments to a select group of investors without a public offer.

But at the center of every compliant preferential allotment is a non-negotiable requirement: a valuation report from an IBBI-registered valuer. Skipping or compromising on this step can render the entire transaction void, trigger penalties under Sections 42 and 450, invite reclassification as a public issue, or attract tax consequences under Section 56(2)(viib) of the Income Tax Act, 1961.

This guide breaks down everything founders, CFOs, company secretaries, and legal advisors need to know about preferential allotment valuation, from legal requirements and methodology selection to step-by-step compliance and tax considerations.

Understanding Preferential Allotment Under Section 62 of the Companies Act, 2013

Preferential allotment, also called a preferential issue, involves issuing shares or convertible securities to a limited set of identified individuals or entities on a non-pro-rata basis. It is structurally different from a rights issue (offered proportionally to existing shareholders) and a public issue (open to the general public).

The legal foundation rests on three key provisions:

- Section 62(1)(c) of the Companies Act, 2013, which permits further issuance of share capital to persons outside the existing equity shareholder base through a special resolution.

- Rule 13 of the Companies (Share Capital and Debentures) Rules, 2014, which prescribes valuation procedures, disclosure obligations, and timelines.

- Section 42 (private placement), which caps allottees at 200 per financial year (excluding qualified institutional buyers) and mandates filing Form PAS-4 as the private placement offer letter.

A special resolution requires 75% shareholder approval, and the Articles of Association must authorize the issuance. Eligible securities include equity shares, fully or partly convertible debentures (FCDs/PCDs), and compulsorily convertible preference shares (CCPS). Non-convertible instruments fall under separate provisions.

Unlisted companies must complete the allotment within 12 months from the date of the special resolution. This mechanism gives startups and growth-stage businesses the flexibility to onboard strategic investors without the regulatory weight of a public listing.

Why Valuation Matters in Preferential Allotment: Beyond Mere Pricing

Valuation in a preferential allotment is not simply about setting a price. It is a governance mechanism that protects multiple stakeholders simultaneously.

Under Rule 13(2)(g), the issue of price of shares or securities, whether for cash or non-cash consideration, cannot fall below the value determined in a registered valuer's report. This rule serves five critical purposes:

- Fairness to Existing Shareholders: It prevents share issuances at artificially low prices that could disproportionately dilute voting rights or economic interests.

- Regulatory Compliance: It reduces the risk of scrutiny by the Registrar of Companies (RoC) or the Ministry of Corporate Affairs.

- Investor Confidence: A professionally prepared valuation signals transparency and makes do diligence smoother.

- Tax Efficiency: Proper valuation aligns with fair market value (FMV) requirements under Section 56(2)(viib), reducing the risk of deemed income on excess premiums.

- Director Protection: It shields the board from allegations of fiduciary breach under Sections 166 and 447.

Done right, valuation transforms a potentially complex compliance exercise into a strategic tool for sustainable capital raising.

Legal Framework for Valuation: Rule 13(2)(g) and Related Provisions

Rule 13(2)(g) of the Companies (Share Capital and Debentures) Rules, 2014 is the cornerstone of valuation compliance. It explicitly requires the issue of price to be determined based on a valuation report from a registered valuer, and the price must not fall below the value so concluded, regardless of whether consideration is in cash or otherwise.

For convertible securities, companies have flexibility in timing: the conversion price may either be fixed at the time of issuance or determined at the time of conversion, provided the valuation report is not older than 60 days before the conversion entitlement date. The chosen approach must be disclosed in the explanatory statement accompanying the special resolution.

Additional Rule 13 requirements include comprehensive disclosures in the explanatory statement covering the objects of the issue, names of allottees, pre- and post-issue shareholding patterns, and the valuation basis. Companies must also file Form PAS-3 with the RoC within 30 days of allotment.

These provisions are aligned with Section 247 of the Companies Act, which governs registered valuers and mandates independence, objectivity, and professional rigor.

Who Qualifies as a Registered Valuer? Eligibility and Responsibilities

A registered valuer is a qualified professional registered with the IBBI under the Companies (Registered Valuers and Valuation) Rules, 2017. For preferential allotments involving securities, the valuer must hold registration in the Securities or Financial Assets (SFA) asset class.

Eligibility criteria include:

- Relevant professional qualifications such as Chartered Accountant, Cost Accountant, or MBA in Finance with requisite experience

- Successful completion of the IBBI valuation examination and mandatory training

- Minimum professional experience as prescribed by IBBI regulations

- Independence from the company, its promoters, directors, and key managerial personnel

The valuer's responsibilities include applying recognized valuation standards (such as ICAI Valuation Standards), documenting assumptions transparently, factoring industry dynamics and risk, and issuing a defensible, detailed report. Valuer independence is not optional. It is fundamental to the transaction's legal validity.

Valuation Methods Employed in Preferential Allotment

Registered valuers select and blend methodologies based on the company's stage, industry profile, and financial history.

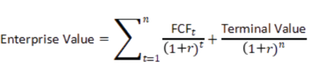

Income Approach: Discounted Cash Flow (DCF) Method

This forward-looking technique projects the company's expected free cash flows and discounts them to present value using an appropriate discount rate, typically the Weighted Average Cost of Capital (WACC).

The DCF formula is:

This method is best suited for startups and high-growth companies where historical earnings do not reflect future potential. Its main limitation lies in sensitivity to assumptions around revenue projections and discount rates.

Market Approach

This method uses comparable company multiples (such as EV/EBITDA or Price/Earnings ratios) or recent comparable transaction data. It is objective where active market data exists but requires careful selection of genuinely comparable peers, with adjustments for differences in size, growth profile, and risk.

Asset-Based Approach: Net Asset Value (NAV)

Calculated as total assets minus total liabilities (both adjusted to fair market values), this method works well for asset-intensive businesses such as manufacturing or real estate companies. It provides a floor valuation but may understate intangible asset value or future earnings potential.

Hybrid Methods

In practice, valuers often use weighted averages, for example, 60% DCF combined with 40% market multiples, to arrive at a balanced conclusion. This approach reduces the subjectivity of any single method and produces a more defensible outcome.

Valuation Considerations for Startups Versus Established Companies

Startups typically rely heavily on DCF, emphasizing scalable business models, user metrics, and projected cash flows given limited historical data. Because of the inherent subjectivity, conservative assumptions and sensitivity analyses are essential.

Mature companies, by contrast, benefit from market approaches using stable EBITDA multiples or asset-based methods, producing more verifiable outcomes. The methodology must match the company's life cycle stage to withstand regulatory and investor scrutiny.

Special Considerations for Valuation of Convertible Instruments

For CCPS, FCDs, or PCDs, the conversion price must comply with Rule 13(2)(h). Companies may choose between two approaches:

1. Upfront Determination: Valuation is locked in at the time of issuance.

2. Deferred Determination: Valuation is carried out not earlier than 60 days before the conversion entitlement date.

The selected approach must be disclosed upfront in the offer documents. This flexibility accommodates shifting valuations in dynamic markets while keeping the transaction fully compliant.

Valuation for Non-Cash Consideration

When shares are issued against assets, intellectual property, or services rather than cash, dual valuations become mandatory: one for the non-cash asset and another for the shares being issued. Rule 13(2)(i) requires the registered valuer to justify both in a comprehensive report. The non-cash consideration must subsequently be accounted for per applicable Ind AS, either capitalized or expensed depending on its nature.

Step-by-Step Compliance Process for Valuation in Preferential Allotment

Step 1: Appoint an independent IBBI-registered valuer at the earliest stage of the process.

Step 2: Furnish comprehensive data including audited financials, business projections, and relevant industry reports.

Step 3: Allow the valuer to conduct thorough due diligence on the company.

tep 4: Obtain the final valuation report detailing the methodology, key assumptions, and concluded fair value.

Step 5: Secure board approval for both the valuation and the proposed issue price, which must be at or above the valued price.

Step 6: Convene a general meeting, pass the special resolution, and ensure all required disclosures are made.

Step 7: Complete the allotment within the stipulated timeline and file the necessary forms with the RoC.

Timely execution prevents lapses and ensures smooth integration with private placement compliances under Section 42.

Essential Contents of a Compliant Valuation Report

A legally defensible valuation report must include:

- Detailed company overview and industry analysis

- Review of historical financial statements and future projections

- Description of the chosen valuation methodology and rationale

- Key assumptions, discount rates, and growth projections used

- Risk factors and sensitivity analysis

- Fair value conclusion supported by detailed calculations

- Valuer's declaration of independence and compliance with applicable standards

Pricing Rules: Differentiating Listed and Unlisted Companies

Unlisted companies must rely on the registered valuer's report under Rule 13 to determine the issue of price.

Listed companies are exempt from this requirement and must instead follow SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 (ICDR). Under ICDR, the price is the higher of:

- The average volume-weighted average price (VWAP) during the 90 trading days preceding the relevant date, or

- The average VWAP during the 10 trading days preceding the relevant date.

The relevant date is generally 30 days before the general meeting date.

Common Pitfalls in Preferential Allotment Valuation and How to Avoid Them

Frequent errors include relying on outdated financial data, using overly optimistic projections, insufficient peer benchmarking, weak documentation, and compromised valuer independence. Any of these lapses can invalidate the allotment, invite regulatory penalties, or trigger tax disputes. Proactive engagement with experienced valuers and legal counsel is the most reliable way to avoid these pitfalls.

Tax Implications of Preferential Allotment Valuation

Valuation directly intersects with Section 56(2)(viib) of the Income Tax Act, which taxes the excess of issue price over FMV as "income from other sources" in the hands of the issuing company, applicable to private companies. Aligning the valuation with Rule 11UA of the Income Tax Rules helps minimize this exposure.

DPIIT-recognized startups enjoy exemptions from angel tax provisions under specified conditions. This makes coordinated tax and corporate planning critical. A valuation that serves both the Companies Act compliance requirement and the Income Tax rule is the most efficient approach.

Penalties for Non-Compliance with Section 62 and Valuation Norms

Violations under Section 42 can attract fines up to Rs. 2 crore or the amount raised, whichever is higher. General defaults invoke Section 450 penalties. Non-compliance can also necessitate refunds with interest and reclassification of the offer as a public issue, exposing the company to broader SEBI oversight and scrutiny.

Practical Tips for Companies Undertaking Preferential Allotment

Engage the registered valuer at the conceptual stage rather than after decisions are made. Maintain exhaustive documentation throughout. Adopt conservative yet realistic assumptions that align with investor term sheets. Obtain concurrent legal review alongside the valuation. Ensuring consistency between valuation inputs and subsequent financial reporting strengthens credibility with auditors, investors, and regulators alike.

Preferential Allotment Versus Alternative Funding Routes: A Comparative Overview

| Funding Method | Valuation Requirement | Flexibility | Speed of Execution | Regulatory Burden |

|---|---|---|---|---|

| Preferential Allotment | Mandatory for unlisted companies (registered valuer) | High | Moderate to High | Moderate |

| Rights Issue | Generally, not required | Limited | High | Low |

| Public Issue (IPO/FPO) | Market-driven (SEBI ICDR) | Low | Low | High |

| ESOPs/Stock Options | Independent valuation often required | Moderate | Moderate | Moderate |

Preferential allotment strikes an optimal balance for companies seeking targeted, efficient capital raising without the overhead of a public offer.

Real-World Use Cases and Strategic Applications

- Startup Series Funding: Issuance of CCPS to venture capitalists at a pre-determined conversion price based on a DCF valuation, ensuring regulatory compliance and investor alignment.

- Promoter Capital Infusion: Allotment to promoters during turnaround phases to strengthen the balance sheet and restore financial confidence.

- Strategic Alliances: Bringing in industry partners via equity swaps supported by dual asset-share valuations, enabling non-cash consideration transactions.

These scenarios illustrate how a defensible valuation enables tailored, value-accretive transactions that hold up to regulatory and investor scrutiny.

Key Challenges in Preferential Allotment Valuation

Market volatility, limited availability of comparable data for early-stage ventures, forecasting uncertainties, and heightened regulatory scrutiny are persistent challenges in this space. Mitigation strategies include robust scenario planning, conservative assumption-setting, and engaging valuers with sector-specific expertise who can defend their conclusions under examination.

Best Practices for Ensuring Seamless Compliance and Value Maximization

Adopt conservative but realistic assumptions and document every input rigorously. Obtain independent legal opinions alongside the valuation report. Ensure consistency between the valuation and the terms set out in shareholder agreements. Periodic review of internal valuation policies further strengthens governance and reduces the risk of disputes at future funding stages.

Conclusion: Valuation as a Strategic Enabler Under Section 62

Preferential allotment valuation under Section 62 of the Companies Act, 2013 is not a box-ticking exercise. It is a strategic imperative that underpins fair, transparent, and sustainable fundraising for unlisted companies.

By mandating IBBI-registered valuer reports, the legal framework protects shareholders, strengthens governance, and builds investor trust. Companies that approach this requirement with professionalism and meticulous compliance position themselves for long-term growth.

Biz Valuations brings 15+ years of experience, 3,500+ certified valuations delivered across 35+ industries, and dual credentials as an IBBI Registered Valuer and SEBI Category I Merchant Banker. Whether you are issuing CCPS to a VC, onboarding a strategic partner, or conducting a promoter infusion, our team delivers defensible, audit-ready valuation reports within 7 to 10 working days.

Mr. Saurobh Barick

Registered Valuer (IBBI) & Valuation Expert

DCF & Fair Market Value Valuations | FEMA, Income Tax & Companies Act | 409A Valuation | M&A, Fundraising valuation | Cross-Border & Startup/Business Valuation | SME IPO AdvisorySaurobh Barick is a Registered Valuer with the Insolvency and Bankruptcy Board of India (IBBI) and a finance professional with over 15 years of experience in valuation and financial advisory services.