Every funding conversation a founder has eventually arrived at a single, high-stakes question: what is your startup worth? But valuation is not one number; it is two. And confusing them can cost founders crores in equity they never intended to give away.

Pre-money vs post-money valuation is one of the most consequential distinctions in startup finance, yet it remains one of the most misunderstood. Whether you are closing a seed round, negotiating a Series A term sheet, or issuing your first ESOPs, knowing the difference is not optional, it is foundational.

For founders building companies in India's fast-growing startup ecosystem home to over 1.59 lakh DPIIT-recognized startups getting this right directly affects ownership control, equity dilution, investor returns, and the long-term trajectory of everything you are building.

This guide walks you through every dimension of pre-money and post-money valuation: what they mean, how to calculate them, how they interact with ESOPs and future rounds, and the strategic mistakes that trip up even experienced founders.

What Is Startup Valuation?

Startup valuation is the process of estimating the economic worth of a young company, primarily in the context of fundraising. Unlike established businesses who evaluated historical profitability, startups are typically valued based on future potential - what the company could become, not just what it is today.

Several factors drive startup valuation in India:

- Market opportunity: Total Addressable Market (TAM) and the startup's realistic share of it

- Product and IP: Innovation depth, proprietary technology, and defensibility

- Founding team: Experience, domain expertise, and execution track record

- Traction metrics: User growth, Monthly Recurring Revenue (MRR), customer retention, and partnerships

- Competitive landscape: Positioning relative to incumbents and emerging rivals

- Scalability and unit economics: Whether the business model improves at scale

At its core, startup valuation is a negotiated outcome for a number that balances a founder's ambition for the future against an investor's assessment of risk. Neither party has a crystal ball, which is why professional, data-backed valuation reports matter.

What Is Pre-Money Valuation?

Pre-money valuation represents the assessed worth of a startup before any new investment is received. It reflects the company's current standing in its assets, traction, team, intellectual property, and growth prospects independent of incoming capital.

Key characteristics of pre-money valuation:

- Does not include the proposed investment amount

- Serves as the negotiating baseline for any funding discussion

- Directly determines the percentage of equity founders will give up

- Reflects the intrinsic, standalone value of the business at that moment

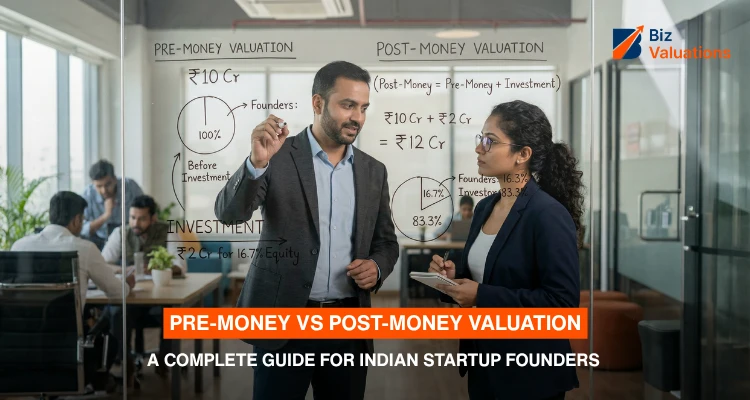

Practical example: If investors collectively agree your startup is worth ₹20 crore before their capital enters the company, your pre-money valuation is ₹20 crore. The actual money hasn't been wired, yet this is purely the agreed-upon worth of what you've already built.

What Is Post-Money Valuation?

Post-money valuation is the company's total value immediately after the investment is completed. It is calculated by adding the incoming investment to the pre-money figure agreed upon during negotiations.

Formula:

Post-Money Valuation = Pre-Money Valuation + Investment Amount

Example:

- Pre-money valuation: ₹20 crore

- Investment raised: ₹5 crore

- Post-money valuation = ₹25 crore

Post-money valuation is the number used to calculate what ownership percentage the investor receives. It directly determines how much of the company you have sold, and it becomes the baseline expectation for your next funding round.

Key Differences Between Pre-Money and Post-Money Valuation

| Aspect | Pre-Money Valuation | Post-Money Valuation |

|---|---|---|

| Timing | Assessed before investment | Calculated after investment closes |

| Includes New Capital | No | Yes |

| Primary Purpose | Negotiation baseline | Determines investor ownership % |

| Impact on Dilution | Sets the equity founders give away | Reflects total company value post-deal |

| Used For | Assessing current business worth | Setting benchmarks for future rounds |

Understanding this table in context is critical. Pre-money determines the price per share at which an investor buys in. Post-money tells everyone founders, investors, future shareholders the total market capitalization of the company after the deal closes.

Why Pre-Money vs Post-Money Valuation Matters for Founders

The difference between these two numbers has a direct, material impact on your ownership stake. Consider two scenarios where the same ₹20 crore figure is quoted differently:

Case 1: ₹20 crore quoted as Pre-Money

- Investment amount: ₹5 crore

- Post-money valuation: ₹25 crore

- Investor ownership: ₹5 crore ÷ ₹25 crore = 20%

Case 2: ₹20 crore quoted as Post-Money

- Investment amount: ₹5 crore

- Pre-money valuation: ₹15 crore

- Investor ownership: ₹5 crore ÷ ₹20 crore = 25%

The same conversation, the same investment amount, but a 5% difference in founder equity. At an eventual exit valuation of ₹500 crore, that 5% gap translates to ₹25 crore - the cost of a single misunderstood word in a term sheet negotiation.

This is why seasoned investors and lawyers are always precise about which valuation they are referencing. Founders must be equally precise and equally informed.

How to Calculate Pre-Money and Post-Money Valuation

There are two primary calculation approaches depending on the information available:

1. From Investment Amount and Ownership Percentage:

Post-Money Valuation = Investment Amount ÷ Investor Ownership % Pre-Money Valuation = Post-Money Valuation − Investment Amount

Example: If an investor puts in ₹5 crore for 20% ownership:

- Post-money = ₹5 crore ÷ 0.20 = ₹25 crore

- Pre-money = ₹25 crore − ₹5 crore = ₹20 crore

2. Price Per Share Calculation:

Price per Share = Pre-Money Valuation ÷ Total Outstanding Shares (before investment)

This per-share price is critical for ESOP plan design, cap table management, and ensuring compliance with Indian regulations - including Rule 11UA under the Income Tax Act and FEMA requirements for cross-border investors.

Running these calculations accurately, with documented assumptions, is the foundation of a credible, investor-ready valuation report.

Factors Influencing Pre-Money and Post-Money Valuation in India

Valuations do not emerge from formulas alone. They are shaped by a combination of business-specific realities and broader market conditions.

Internal Factors:

- Founding team quality and domain depth

- Revenue growth trajectory, gross margins, and cash burn rate

- Product-market fit and strength of intellectual property

- Customer acquisition cost (CAC), lifetime value (LTV), and retention metrics

External Factors:

- Total market size and the pace of sector growth

- Industry momentum - fintech, SaaS, deep tech, and D2C have commanded premium multiples in India

- Macroeconomic conditions and the prevailing funding climate

- Comparable deals closed recently in the same sector

India's startup fundraising environment in 2025 saw $10.5–11 billion raised across 1,518 deals. Sector-specific multiples have shifted substantially. Pre-money valuations that made sense in 2021's frothy market look very different under today's more disciplined investor scrutiny making an independent, data-backed valuation more important than ever.

Common Mistakes Indian Founders Make

Even well-informed founders fall into predictable traps. Awareness of these pitfalls is the first layer of protection:

- Conflating the two terms: Treating pre-money and post-money interchangeably in verbal negotiations without documenting which one is meant creates disputes that are difficult and expensive to unwind.

- Accepting overinflated valuations: A headline valuation that seems flattering today can become a ceiling in the next round, forcing a down round that damage's credibility and team morale.

- Ignoring term sheet economics: Founders sometimes fixate on the valuation number while overlooking clauses that matter equally liquidation preferences, anti-dilution rights, pro-rata rights, and board seat provisions.

- Skipping professional valuation support: Entering a negotiation without an independent, third-party valuation report puts founders at an informational disadvantage relative to experienced investors who run valuation models daily.

Each of these mistakes is avoidable. Preparation, clarity, and the right advisory support are the countermeasures.

How Pre-Money and Post-Money Valuation Affect ESOPs and Future Rounds

The post-money valuation your company carries after a funding round has consequences that extend well beyond the current deal.

Impact on ESOPs: The exercise (strike) price of employee stock options is typically set at or near Fair Market Value (FMV) at the time of grant. A higher post-money valuation raises the FMV, which increases the strike price employees must pay to exercise options. For early employees, high strike prices can meaningfully reduce the financial upside of their equity potentially hurting your ability to attract and retain top talent.

Impact on future rounds: Post-money valuation sets the floor that your next investor round must clear. If your Series A post-money was ₹100 crore, your Series B investors will expect the business to be worth materially more and they will scrutinize whether the fundamentals support that trajectory. Overvaluation at one stage compresses the room to man oeuvre at the next, and in the worst case, triggers a down round where shares are issued at a lower price than the previous round signaling distress to the market and existing investors.

Best Practices for Founders

A few disciplines, consistently applied, can significantly improve valuation outcomes across every funding conversation:

- Always confirm which valuation is being discussed - ensure every conversation and written document explicitly states whether a figure is pre-money or post-money

- Model dilution scenarios before you negotiate - run the numbers across multiple investment amounts and ownership percentages to understand the full range of outcomes

- Use multiple valuation methodologies - the Venture Capital Method, Scorecard Method, and Comparable Transactions approach each illuminate different dimensions of value; professional valuers use all three

- Priorities deal terms alongside headline valuation - a slightly lower valuation with founder-friendly terms often produces better long-term outcomes than a higher number with onerous investor protections

- Maintain a clean, updated cap table - clarity on existing ownership is essential before any new round, and confusion here creates negotiation friction and legal risk

Why Professional Valuation Services Are Important

An accurate, independently prepared valuation report does several things that a founder's own estimates cannot.

It builds investor confidence by providing a data-backed, methodology-driven figure that stands up to due diligence. It ensures compliance with India's regulatory frameworks including Section 56 and Section 50CA of the Income Tax Act, which carry tax consequences for shares issued at a discount to FMV, and FEMA regulations governing cross-border share transactions. It provides defensible documentation for audit, SEBI filings, and regulatory submissions.

Beyond compliance, professional valuers provide sophisticated financial modelling, scenario analysis, and direct negotiation support, giving founders both the numbers and the context to use them effectively.

Why Biz Valuation Is the Preferred Partner for Indian Startups

Biz Valuations has built its reputation on delivering precise, regulation-compliant valuations that founders can take into any investor's conversation with confidence. Here is what distinguishes the firm as a partner for Indian startups:

- Specialized expertise in early-stage and growth-stage company valuation, with an understanding of what investors at each stage actually scrutinize

- Investor-ready reports compliant with the Companies Act 2013, Income Tax Act, FEMA/FDI regulations, and Ind-AS/IFRS standards

- Deep familiarity with India's startup ecosystem including DPIIT exemptions, angel tax implications, and ESOP structuring dynamics

- Advanced financial modelling including DCF analysis, Hybrid Methods, DLOM analysis, and Volatility Benchmarking for complex capital structures

- Fast turnaround times 7–10 working days aligned with funding timelines that do not wait

- Customized, affordable solutions for both bootstrapped startups and VC-backed companies at every stage

- All valuation reports are certified by an IBBI Registered Valuer and SEBI Category I Merchant Banker as required by the client's specific regulatory mandate

Biz Valuations has delivered 3,500+ certified valuations across 35+ industries, with over ₹40 billion in total valuation work - providing the market-comparable depth that produces accurate, defensible reports.

Conclusion

Pre-money vs post-money valuation is not a technicality to be delegated or glossed over. It is the arithmetic of your ownership, and every percentage point of equity has a monetary value that compounds over the lifetime of your company.

In India's increasingly sophisticated startup ecosystem, where investors arrive at the table with detailed models and deep sector data, founders who understand valuation dynamics negotiate from strength. Those who don't often discover the cost of ambiguity only after the term sheet is signed.

Biz Valuations exist to ensure that it never happens to the founders it works with. From pre-seed compliance certificates to pre-IPO fairness opinions, the firm delivers accurate, regulation-compliant, and strategically defensible valuations so founders can focus on building, while the numbers are in expert hands.

If your next funding round is on the horizon, start with clarity. Understand your valuation both before and after investment. Then negotiate accordingly.

Frequently Asked Questions (FAQs)

Mr. Saurobh Barick

Registered Valuer (IBBI) & Valuation Expert

DCF & Fair Market Value Valuations | FEMA, Income Tax & Companies Act | 409A Valuation | M&A, Fundraising valuation | Cross-Border & Startup/Business Valuation | SME IPO AdvisorySaurobh Barick is a Registered Valuer with the Insolvency and Bankruptcy Board of India (IBBI) and a finance professional with over 15 years of experience in valuation and financial advisory services.