India's business environment is evolving rapidly and with that evolution comes a question every founder, CFO, and business owner must answer with precision: what is my business, asset, or share actually worth?

Fair Market Value (FMV) is that answer. Whether you are a startup founder preparing for a funding round, a CFO managing ESOP grants, a promoter structuring an M&A deal, or a finance professional handling tax filing, FMV is the foundation on which sound decisions, regulatory compliance, and long-term value creation rest.

The landscape shifted when the Angel Tax under Section 56(2)(viib) was abolished effective April 1, 2025 - but FMV did not become less relevant. Today, it governs ESOP taxation, capital gains under Section 50CA, gift tax liability, financial reporting under Ind AS 113, and dispute resolution in courts and tribunals.

This 2026 guide gives Indian entrepreneurs and finance professionals a clear, actionable understanding of FMV covering the definition, core principles, valuation methods, India's current regulatory framework including Rule 11UA, real-world examples, influencing factors, common mistakes, and why professional expertise is non-negotiable.

What Exactly Is Fair Market Value (FMV)?

Fair Market Value is the price at which an asset or business interest would change hands between a hypothetical willing buyer and willing seller both reasonably informed about all relevant facts, acting freely without coercion, and transacting in an open, competitive market.

FMV is not what you think your business is worth. It is not the historical cost of an asset, and it is not what it would cost to rebuild it. FMV is market-oriented and forward-looking it reflects current economic realities, prevailing industry dynamics, and what an objective buyer would actually pay today.

Think of FMV as the price that would emerge at a transparent, well-run auction. It eliminates personal biases, related-party distortions, and forced-sale pressures leaving behind an objective, defensible number that holds up before tax authorities, auditors, investors, and courts.

In the Indian regulatory context, FMV draws from internationally accepted valuation standards while aligning with the Income-tax Act 1961, the Companies Act 2013, and Indian Accounting Standards (Ind AS). It applies across unquoted equity shares, immovable property, jewellery, businesses as going concerns, and intangible assets including IP, brands, and goodwill.

Why FMV Matters More Than Ever for Indian Businesses in 2026

FMV directly shapes your tax liability, fundraising terms, deal structure, financial statements, and ability to resolve disputes. Here is its practical impact across five critical areas.

1. Tax Compliance and Capital Gains

Under Section 50CA, if unquoted shares are transferred at a price below FMV, tax authorities treat the FMV as the full consideration for capital gains computation. This anti-avoidance provision applies regardless of whether the transfer is to a related party or a third party. Rule 11UA, now consolidated under the new Income-tax Rules 2026, provides the prescribed methodology. An incorrect or unsupported FMV can trigger notices, adjustments, and penalties of up to 200% of tax evaded.

Gift taxation under Section 56(2)(x) creates another FMV exposure: receiving property significantly below FMV may attract tax in the recipient's hands. A professionally certified FMV report provides the documentation needed to defend against such claims.

2. ESOPs and Employee Incentive Plans

ESOP taxation under Section 17(2) treats the difference between FMV on the exercise date and the exercise price as a taxable perquisite in the employee's salary. Employers must determine FMV using merchant banker reports or IBBI-registered valuer assessments. With Angel Tax abolished, ESOPs have become an even more attractive tool for talent retention, but getting the FMV right is essential to avoid downstream tax friction for employees.

3. Mergers, Acquisitions, and Fundraising

In M&A, FMV is the bedrock of negotiations, fairness opinions, and deal pricing. For foreign investment transactions, FMV ensures FEMA compliance required for every FC-GPR and FC-TRS filing. For cross-border share transfers above USD 5 million, a SEBI Category I Merchant Banker must certify the FMV, a specific credential that most valuation firms cannot provide.

4. Financial Reporting and Investor Confidence

Ind AS 113 mandates fair value measurement for financial assets, liabilities, and certain non-financial assets. Transparent, properly documented FMV strengthens balance sheet credibility, supports credit ratings, and for companies in IPO pipelines directly influences how public market investors receive the offering.

5. Litigation, Disputes, and Insolvency Proceedings

Courts, tribunals, and insolvency professionals rely on FMV in shareholder disputes, family business succession matters, divorce proceedings involving business assets, and NCLT matters under the IBC. An independent FMV report from a credentialed valuer often becomes the decisive evidence, and an unsupported internal estimate rarely survives legal challenge.

FMV is the common language of value across India's entire regulatory ecosystem.

Core Principles That Define Fair Market Value

Four foundational principles govern every legitimate FMV determination:

1. Willing Buyer and Willing Seller - Neither party faces coercion. Both are motivated by rational economic interest.

2. Arm's Length Transaction - The deal occurs between entirely independent parties with no relationship that could distort pricing.

3. Full Knowledge and Information - Both parties have access to all material facts: financials, growth projections, risk factors, and market position.

4. Open Market Conditions - The valuation reflects what a competitive, transparent market would yield free from artificial restrictions or forced timelines.

These principles distinguish a true FMV from a subjective internal estimate or a rushed compliance certificate.

Proven Methods to Determine Fair Market Value

No single formula applies universally. Method selection depends on asset type, data availability, and valuation purpose. Indian professionals typically apply one or a combination of four primary approaches, cross-verifying results for robustness.

1. Market Approach (Comparable Company or Transaction Method)

This benchmarks the subject asset against recent sales of genuinely comparable assets.

- Listed shares: Prevailing market price, adjusted for liquidity and control of premiums or discounts.

- Real estate: Recent registered sales of comparable properties, adjusted for location, size, and condition.

- Businesses: EV/EBITDA, Price-to-Earnings, or EV/Revenue multiples from comparable listed peers or recent private transactions applied to the subject company's financials.

- Strength: Highly market reflective.

- Limitation: Requires genuinely comparable data, which can be scarce for unique or early-stage Indian startups.

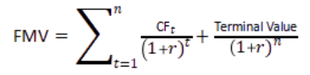

2. Income Approach (Discounted Cash Flow and Capitalization Methods)

Value is derived from expected future economic benefits, discounted to present value using an appropriate risk-adjusted rate.

Where CF_t is the projected free cash flow in period t, r is the WACC or appropriate discount rate, and Terminal Value is typically computed using the Gordon Growth Model.

Widely used for startups, service businesses, IP-rich companies, and rental properties. The quality of a DCF valuation depends entirely on the reasonableness of the underlying assumptions, which is why independent, professional preparation is critical.

3. Cost Approach (Replacement or Reproduction Cost)

This estimates the cost of recreating the asset from scratch, adjusted downward for physical deterioration, functional obsolescence, and economic obsolescence. Most appropriate for tangible assets of plant and machinery, specialized infrastructure, or industrial equipment where no active resale market exists.

4. Net Asset Value (NAV) or Break-Up Method

The default method under Rule 11UA(1)(c)(b) for FMV of unquoted equity shares for tax purposes. The formula is:

FMV per share = [(A + B + C + D − L) × PV] / PE Where

- A = Adjusted book value of assets (excluding certain items).

- B = Open market value of jewellery/artistic works (registered valuer).

- C = FMV of quoted/unquoted securities.

- D = Stamp-duty value of immovable property.

- L = Adjusted liabilities (excluding equity, reserves, etc.).

- PV = Paid-up value of the specific share class.

- PE = Total paid-up equity capital.

Best suited for asset-heavy companies and holding entities. For growth-stage startups with minimal tangible assets, it often significantly understates economic value — making DCF or market-based approaches far more appropriate.

Professional practitioners frequently triangulate across two or more methods, using convergence or divergence of results to stress-test assumptions and arrive at a defensible conclusion.

FMV Under Current Indian Tax and Regulatory Laws: 2026 Update

Rule 11UA

Rule 11UA remains the primary framework governing FMV for unquoted equity shares, jewellery, archaeological items, and immovable property. The new Income-tax Rules 2026 consolidate related provisions including former Rules 11UAA and 11UAB into unified guidance while preserving core methodologies. A 10% safe harbour variation is recognized in select contexts, providing a buffer against minor valuation of differences being treated as taxable events.

Section 50CA

If unquoted shares are transferred at a price below their Rule 11UA FMV, Section 50CA deems the FMV to be the full sale consideration for the transferor's capital gains computation. This has no exceptions for related-party transfers or restructuring transactions; a contemporaneous valuation report is essential before completing any such transfer.

Angel Tax Abolition

Section 56(2)(viib) was fully removed from effective FY 2025-26. Companies can now issue shares at premiums above FMV without triggering tax in the company's hands. However, FMV documentation remains best practice: audit trails matter, and every historical transaction comes under scrutiny as companies approach IPO or acquisition.

ESOP and Perquisite Taxation

FMV certification remains mandatory for computing taxable perquisite on ESOP exercise under Section 17(2). IBBI-registered valuers and SEBI-registered Merchant Bankers are recognized by authorities for this certification.

Companies Act, IBBI, FEMA, and SEBI

Section 247 of the Companies Act 2013 mandates registered valuers for valuations in mergers, buyouts, and insolvency proceedings. FEMA's FDI valuation rules require FMV certification for every inbound and outbound share transfer, with a SEBI Category I Merchant Banker mandatory for transactions exceeding USD 5 million. SEBI's regulations on preferential allotments, open offers, buybacks, and delisting all reference independent FMV.

Ind AS 113: Fair Value Hierarchy

Ind AS 113 establishes a three-level hierarchy for fair value measurement:

- Level 1: Quoted prices in active markets for identical assets.

- Level 2: Observable inputs other than quoted prices.

- Level 3: Unobservable inputs based on management assumptions — requires detailed disclosure and is the relevant category for most unlisted company assets.

Staying current with CBDT notifications and IBBI guidelines is essential for maintaining valid valuation positions.

Real-World Examples: How FMV Works in Practice

Startup ESOP Grant:

A Bengaluru fintech grants ESOPs at ₹80 per share. At exercise, an independent DCF and comparable method valuation establishes FMV at ₹180. The employee recognizes ₹100 per share as a taxable perquisite. If the company had used an internally estimated ₹120 and the tax officer later determines ₹180, the employee faces a demand notice on unreported perquisite income plus interest and penalty. A credentialed FMV at the time of exercise eliminates this risk entirely.

Commercial Property Transaction:

A Mumbai commercial property sells at ₹4 crore. The stamp duty circle rate is ₹5.2 crore and an independent valuer's FMV is ₹5.5 crore. Under Section 56(2)(x), the ₹1.5 crore difference between the purchase price and the higher of stamp duty value or FMV may be treated as income in the buyer's hands. A contemporaneous valuation report explaining the gap provides the documentation to defend the transaction price.

Intra-Group Share Transfer:

An unlisted manufacturing company transfers shares to a group entity below the Rule 11UA NAV-computed FMV. Section 50CA automatically triggers capital gains on the difference — even if no real economic gain occurred. This underscores why a contemporaneous Rule 11UA report is non-negotiable before completing any intra-group transfer.

M&A Negotiation:

A Delhi-based logistics firm is acquired using a blended NAV-plus-DCF valuation reflecting an 8x EV/EBITDA multiple consistent with recent comparable sector deals. Both boards rely on this independently established figure as a defensible deal price, and the fairness opinion built on this FMV helps the target company's directors discharge their fiduciary responsibility.

Key Factors That Influence FMV in the Indian Context

FMV is dynamic. Major drivers include:

- Macroeconomic conditions RBI interest rate movements directly affect DCF discount rates; inflation erodes real cash flows; GDP growth shapes sector risk appetite.

- Industry-specific trends sectors with regulatory tailwinds (renewable energy, EVs under PLI schemes) command higher multiples than those facing structural disruption.

- Geography and demand-supply dynamics Tier-1 city assets command premiums; Bengaluru's startup corridor attracts different investor interest than comparable non-metro firms.

- Asset quality and technological relevance physical condition, remaining useful life, and obsolescence risk drive cost-approach adjustments; IP and technology quality can be the decisive value driver for knowledge businesses.

- Regulatory shifts GST changes, environmental norms, labor law amendments, and sector-specific policy developments all shift earnings projections and risk-adjusted discount rates.

- Comparable transaction data and market liquidity in active markets, comparables are plentiful; in niche or illiquid private markets, finding genuinely comparable transactions requires deep market knowledge.

- Geopolitical and global sentiment for companies with export revenue or foreign investor interest; global risk appetite becomes a material FMV input.

In 2026, India's digital economy growth, sustainability reporting mandates, easing foreign investment norms, and the post-Angel-Tax fundraising environment continue to shape valuations in ways that make current, updated analysis essential.

Common Mistakes to Avoid in FMV Estimation

1. Using outdated financials or ignoring post-balance sheet events: FMV is always dated to a specific valuation date. Financial inputs must be current for a major customer to win, regulatory approval, or credit event after the balance sheet date is material.

2. Cherry-picking comparables without proper adjustments: Selecting only high-multiple comparable companies without adjusting for differences in size, geography, profitability, and growth rate inflates FMV. Auditors and tax officers are experienced at identifying cherry-picked sets.

3. Confusing book value with FMV: Book value reflects historical cost minus depreciation it tells you nothing about what a willing buyer would pay today. For growing businesses, FMV routinely exceeds book value by multiples.

4. Using aggressive DCF assumptions without sensitivity analysis: A model built on over-optimistic revenue growth or an unjustifiably low discount rate produces an artificially high FMV. Without scenario testing, the result is not defensible under audit.

5. Skipping professional certification for regulated transactions: In-house estimates are appropriate for internal planning. They are not appropriate for ESOP grants, share transfers, M&A filings, or financial reporting valuations where statutory requirements mandate a credentialed, independent valuer.

Why Professional Valuation Expertise Is Non-Negotiable

FMV determination combines technical rigor and professional judgment. It requires deep regulatory knowledge across Income Tax, Companies Act, SEBI, FEMA, and Ind AS simultaneously plus sector-specific insight and the impartiality that only an independent expert can credibly provide.

IBBI-registered valuers (Securities and Financial Assets class) and SEBI Category I Merchant Bankers are the two legally recognized professional categories for certified FMV determinations in India. Their reports carry statutory weight holding up in tax assessments, audit reviews, NCLT proceedings, and investor due diligence.

In-house estimates, while useful for planning, rarely survive regulatory scrutiny and expose directors to personal liability if a transaction is later challenged. A report from a registered professional demonstrates good faith compliance and shifts accountability to the certified expert.

Beyond compliance, a skilled valuer adds strategic value: selecting the right methodology, stress-testing assumptions, structuring the valuation for maximum defensibility, and providing advisory support through auditor queries and regulatory representations.

Why Biz Valuations Stands Out as a Trusted Partner

When accuracy and compliance are non-negotiable, credentials and track record matter. Biz Valuations has built its reputation through consistent delivery across thousands of assignments and every major Indian regulatory framework.

- Dual Regulatory Authority: IBBI-registered valuers (Securities and Financial Assets class) and SEBI Category I Merchant Bankers on the team, covering every mandatory valuation context: Rule 11UA certificates, ESOP reports, large FDI certifications, SEBI open offer valuations, and IBC insolvency assignments.

- Proven Scale: 3,500+ certified valuations across startups, manufacturing, fintech, real estate, and corporate groups spanning 35+ industries. This depth of comparable transaction experience strengthens every new report.

- Full Regulatory Alignment: Every report complies with Indian Valuation Standards, Rule 11UA requirements, Ind AS 113 fair value hierarchy, and the latest CBDT notifications.

- Audit-Ready Methodology: Reports are accepted by Big 4 audit teams and withstand tax department scrutiny. Detailed assumptions of workpapers, sensitivity analyses, and clear methodology explanations are built to handle assessment challenges.

- Holistic Advisory Support: Beyond the report, the team assists with auditor query responses, tax department representations, and transaction structuring advisory.

- Customized, Industry-Specific Solutions: Methodologies tailored to the specific business model, sector dynamics, and regulatory purpose not one-size-fits-all templates.

Practical Tips for Effective FMV Management

- Maintain robust, audited financial records and update them regularly to data quality directly determines report quality.

- Track sector comparables and macroeconomic indicators proactively to anticipate how FMV will move ahead of planned transactions.

- Engage qualified valuers early before term sheets are signed, so valuation informs transaction structuring rather than merely validating a predetermined price.

- Document all assumptions, methodologies, and sensitivity analyses transparently. A valuation that cannot explain its assumptions is not defensible.

- Review FMV periodically after material events: significant customer wins, regulatory approvals, leadership changes, or new funding rounds.

- Stay current with CBDT and IBBI notifications, regulatory changes can alter applicable methodology or safe harbour limits, creating unexpected compliance exposure if valuations are based on outdated rules.

The Bottom Line: FMV as a Strategic Business Asset

Fair Market Value is far more than a compliance number. In 2026's Indian business environment shaped by Angel Tax abolition, a record IPO pipeline, accelerating digital growth, and tightening enforcement across IBBI, SEBI, FEMA, and Income Tax a well-documented, professionally certified FMV positions your business to minimize risk, optimize deal terms, attract institutional capital, and build sustainable value.

Whether the context is a tax filing, ESOP grant cycle, M&A negotiation, fundraising round, or board-level strategic review, FMV done right fosters confidence among stakeholders and regulators alike. By combining sound methodology, current regulatory alignment, and genuine professional expertise, Indian businesses can turn valuation from a compliance obligation into a genuine competitive advantage.

Frequently Asked Questions (FAQs)

Mr. Saurobh Barick

Registered Valuer (IBBI) & Valuation Expert

DCF & Fair Market Value Valuations | FEMA, Income Tax & Companies Act | 409A Valuation | M&A, Fundraising valuation | Cross-Border & Startup/Business Valuation | SME IPO AdvisorySaurobh Barick is a Registered Valuer with the Insolvency and Bankruptcy Board of India (IBBI) and a finance professional with over 15 years of experience in valuation and financial advisory services.